The American subprime mortgage crisis was a multinational financial crisis that occurred between 2007 and 2010, contributing to the 2008 financial crisis. It led to a severe economic recession, with millions becoming unemployed and many businesses going bankrupt. The U.S. government intervened with a series of measures to stabilize the financial system, including the Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA).

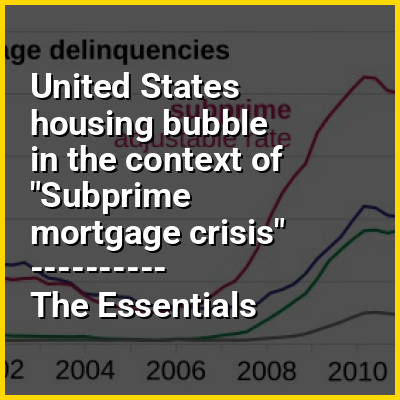

The collapse of the United States housing bubble and high interest rates led to unprecedented numbers of borrowers missing mortgage repayments and becoming delinquent. This ultimately led to mass foreclosures and the devaluation of housing-related securities. The housing bubble preceding the crisis was financed with mortgage-backed securities (MBSes) and collateralized debt obligations (CDOs), which initially offered higher interest rates (i.e. better returns) than government securities, along with attractive risk ratings from rating agencies. Despite being highly rated, most of these financial instruments were made up of high-risk subprime mortgages.