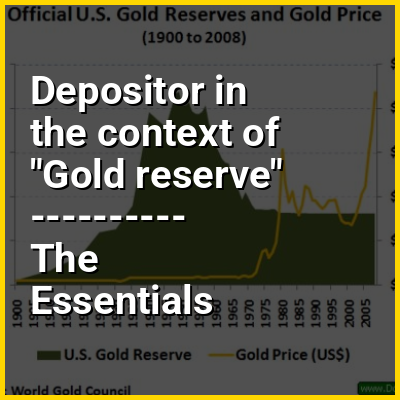

A gold reserve is the gold held by a national central bank, intended mainly as a guarantee to redeem promises to pay depositors, note holders (e.g. paper money), or trading peers, during the eras of the gold standard, and also as a store of value, or to support the value of the national currency.

The World Gold Council estimates that all the gold ever mined, and that is accounted for, totalled 190,040 metric tons in 2019 but other independent estimates vary by as much as 20%. At the price of $40 per gram reached on 16 August 2017, one metric ton of gold has a value of approximately $40.2 million. The total value of all gold ever mined, and that is accounted for, would exceed $7.5 trillion at that valuation and using WGC 2017 estimates.